With more than 21 million LLCs currently operating in the U.S., it’s clear that this business structure has become a go-to choice for entrepreneurs and small business owners alike. In comparison, there are only about 1.7 million traditional C-Corporations and approximately 23 million sole proprietorships. IRS statistics show a year over year increase in domestic LLCs since 2004, underscoring their growing appeal. But many business owners still wonder: when is the right time to get an LLC?

This guide explores the benefits and limitations of forming an LLC, compares it to other entity types, and helps you decide if this is the right step for your Pennsylvania business.

Why LLCs Are So Popular

Typically, C-Corporations, or S-Corporations”, are often the first to come to mind. The “C” and the “S” refer to IRS Code Sections. C corps feature a double taxation – one tax at the company level and another tax on profits distributed to shareholders. This double tax is why many people consider S corps, which has only one level of tax. But there are restrictions on ownership of S corps, which is why LLCs easily slide into the picture.

LLCs are popular because they are not only extremely easy to form, but they are also easy to run. They make taxes much more streamlined, require less corporate formalities, provide for greater flexibility, and they have limited liability for owners too.

Benefits of Forming an LLC

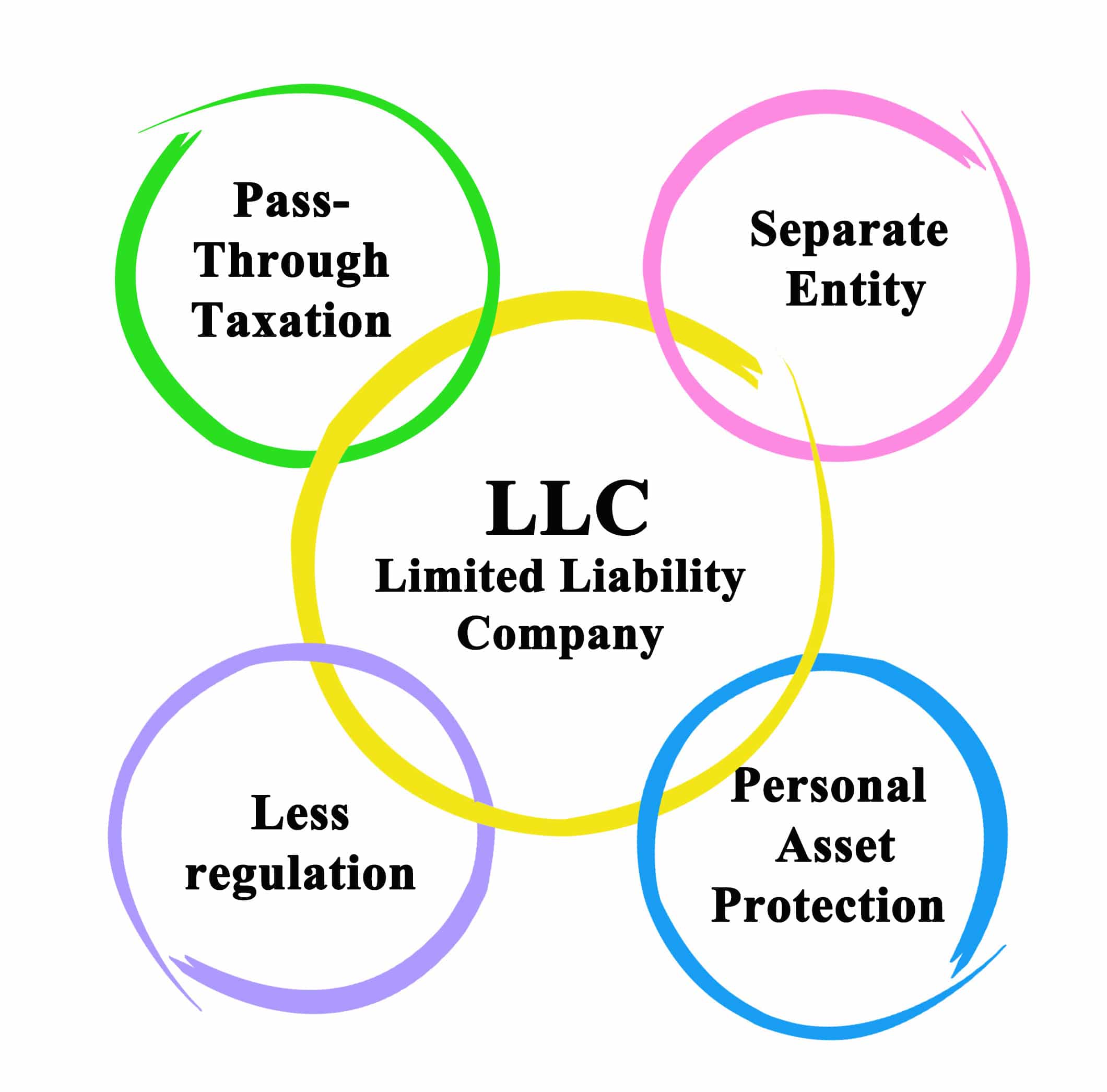

A limited liability company, or LLC, is a hybrid business structure that combines the simplicity, flexibility, and tax advantages of a partnership with the liability protection of a corporation. An LLC gives you the benefits of a corporation without the many hassles. Some of the most important benefits are outlined below.

1. Limited personal liability

When you form a corporation or an LLC it becomes a separate legal entity apart from its owners. This means that the business itself can own assets, enter into contracts, and is liable for its own debts.

If the corporation or LLC cannot pay its debts, creditors can normally only go after the assets owned by the company and not the personal assets of the owners. However, the business owner can also be held responsible for corporate or LLC debts in certain situations.

2. Tax Flexibility

Unlike corporations, LLCs aren’t locked into a single tax structure. They can choose to be taxed as a sole proprietorship, partnership, S-Corp, or C-Corp. This flexibility allows business owners to select the most advantageous tax treatment based on current income, expenses, and future goals.

3. Simple Setup and Fewer Formalities

LLC formation is often quicker and less burdensome than forming a corporation. In Pennsylvania, LLCs avoid many formal requirements like board meetings, shareholder votes, and complex filings. This makes ongoing compliance much more manageable.

4. There is more ownership and management flexibility

LLCs can be member-managed or manager-managed, depending on how you want to structure decision-making. The details are typically outlined in an operating agreement, which is easier to customize than a corporation’s bylaws.

Unlike S-Corps, LLCs have no limits on the number or type of owners. You can have foreign owners, corporate members, or even single-member LLCs—all with the benefit of pass-through taxation if desired.

What are the challenges and disadvantages of an LLC?

Even though there are quite a few benefits to an LLC, there are some drawbacks as well. For small businesses, there are not many. The LLC is the entity of choice in most situations. However, in Pennsylvania, it is often not the entity of choice to hold and develop real estate that may appreciate significantly in value. Also, if you intend to raise significant outside capital, many investors also prefer traditional corporations.

No separate tax designation

As noted above, the IRS does not have a separate tax designation for LLCs. This means that LLCs must choose whether they want to be taxed like a partnership or like a corporation. By default, LLCs are taxed like partnerships, meaning LLC profits are passed through to the owners and taxed with the owners’ income taxes. If LLCs complete proper IRS forms on time, they can choose to be taxed like corporations, meaning they are taxed twice: once on profits at the corporate level and again on any distributions at the individual ownership level.

Should your company be an LLC?

Should your company be an LLC?

It depends, because every situation is different. Choosing the proper entity form can make or break a new business. There are several choices: C-Corporation (C-Corp), S-Corporation (S-Corp), Limited Liability Company (LLC), Limited Liability Partnership (LLP) or a Partnership. There are advantages and disadvantages to operating under each of these forms. In choosing the proper form, it is important to consider several tax and non-tax factors, including liability, taxation, management, and ownership structure.

If you are going to create a business entity, LLCs have a lot of advantages over other similar types of businesses. If you are unsure about whether creating an LLC is a good option for you, ask a lawyer at Fitzpatrick Lentz & Bubba. If you are ready to incorporate your business as an LLC, S-Corp, C-Corp, or Nonprofit, let our team help make the incorporation process as simple and efficient as possible.